At A Glance

SaaS is under structural pressure – AI agents can bypass SaaS interfaces entirely, while enterprise buyers consolidate stacks and question which subscriptions they still need.

Operational/industrial tech has inverted AI-dynamics compared to SaaS – The same AI compressing SaaS is expanding what’s possible in physical operations, where problems remain hard and data is proprietary.

Domain expertise + AI = extremely durable moat for operational tech companies – A generalist can build anomaly detection, but only a 15-year veteran in metal fabrication knows what a specific vibration signature actually means.

Flywheel effect deepens defensibility – Deployments generate proprietary data that sharpens models, earning deeper integration, which generates richer data, a cycle new entrants can’t shortcut with compute.

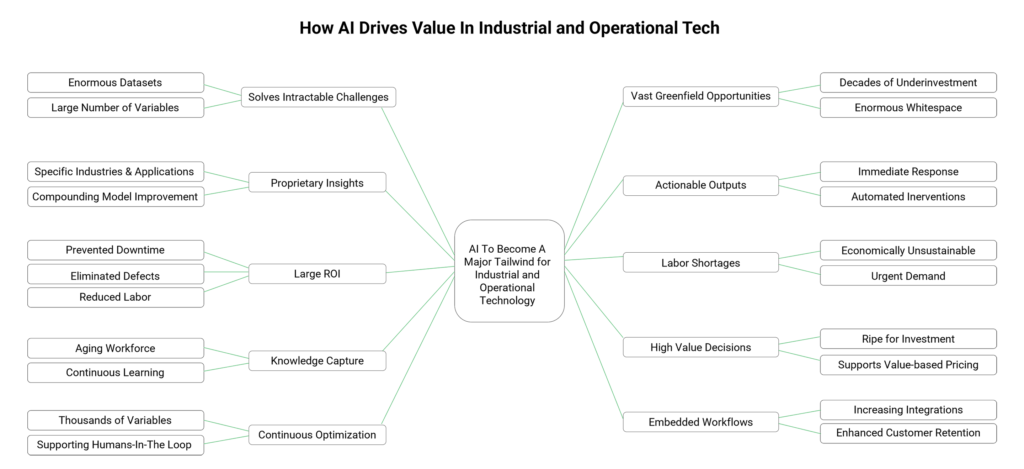

The deployment gap is massive – The range of AI-enabled use cases in operational and industrial tech is almost entirely unpenetrated. The gap between what is possible and what is deployed is extremely large.

ROI is large and measurable – Operational AI delivers discrete, auditable outcomes: reduced labor costs, avoided downtime, reduced scrap, and permanent unit economics gains.

Retiring skilled workers are a hidden tailwind – AI that captures the institutional knowledge of an aging industrial and operational tech workforce represents an entirely new category of value.

Edge-AI Hardware Drives Retention – Most industrial and operational tech use cases will require edge AI capabilities – often leveraging proprietary hardware placed in customer environments – driving a very high level of customer and revenue retention.

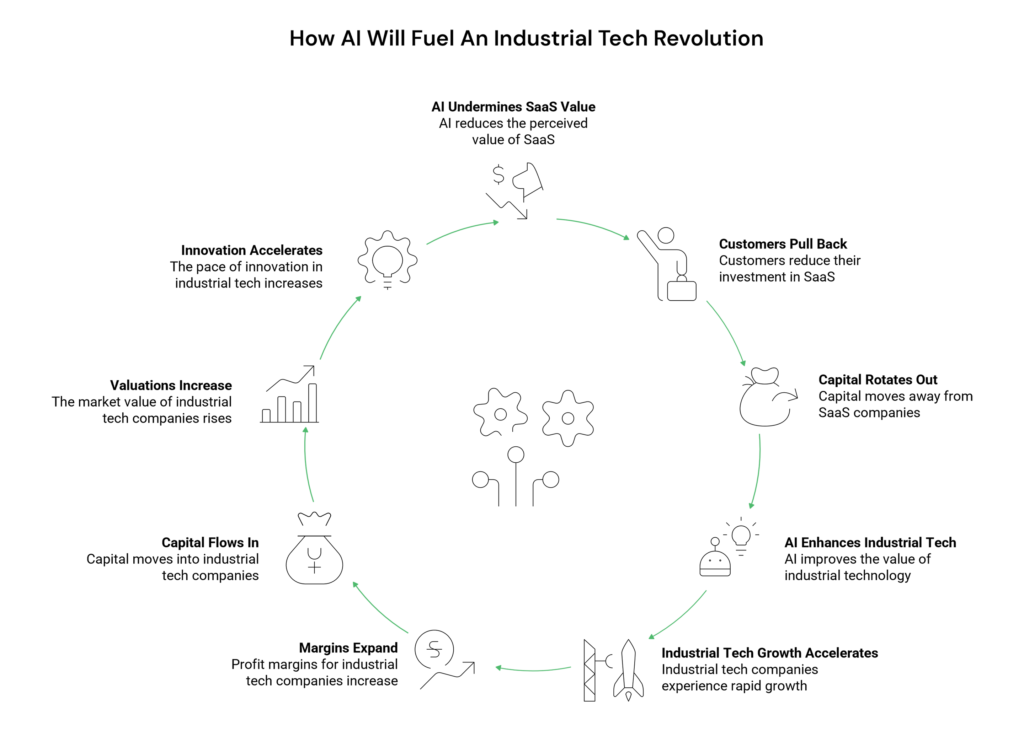

Capital rotation is coming – As AI-enhanced operational and industrial tech sees its value increase, margins will expand, growth will accelerate, and investment is expected to shift meaningfully away from SaaS toward operational technology.

The AI-Driven Revolution Is Getting Started in Industrial and Operational Tech

While SaaS valuations deflate under AI-native competition, a quieter AI-driven revolution is gaining momentum across manufacturing lines, distribution centers, retail floors, and critical infrastructure; anywhere operations meet the physical world. The result is going to be transformative for industrial and operational tech companies and investors, as value propositions expand, revenue and margins increase, and capital rotates out of SaaS and into these long-established but newly discovered tech industries.

For fifteen years, enterprise software sold a compelling promise: encode expertise into software, distribute it at zero marginal cost, and collect recurring revenue indefinitely. It was a good model. It attracted enormous capital. And it is now being stress-tested by the very force the industry claimed as its own. AI agents can perform a striking share of what many SaaS products do, not by replacing their interfaces, but by bypassing them entirely. When outcomes matter more than interfaces, interfaces become commodities. That is a structural problem, not a cyclical one.

The compression is coming from both directions at once. AI-native startups are entering legacy SaaS categories with cost structures and capabilities incumbents cannot match, while enterprise buyers are actively consolidating vendor stacks, asking hard questions about which subscriptions they actually need. Meanwhile, the core SaaS markets for productivity software, HR platforms, and sales automation have simply matured. Fifteen years of aggressive expansion leaves limited whitespace. What looked like durable moats were, in many cases, switching costs waiting to be dissolved.

The same AI capabilities that are compressing SaaS are expanding the frontier of what is possible in operational and industrial technology, and the dynamics are almost precisely inverted.

The same AI capability that is compressing SaaS is expanding the frontier of what is possible in operational and industrial technology, and the dynamics are almost precisely inverted. Where SaaS problems were largely solved and being commoditized, operational problems remain genuinely hard. Where SaaS data could often be approximated or regenerated, operational data is proprietary and inseparable from the physical environment that produced it. Where SaaS switching costs were eroding, the switching costs embedded in physical infrastructure and domain expertise are durable.

Operational Tech’s Presence is Generally Underestimated

Operational technology spans a wider range of industries than the term often implies. It is the computer vision system in a grocery distribution center that identifies picking errors and reroutes orders before they ship. It is the AI model running on a continuous casting line that detects surface defect precursors in molten steel and adjusts cooling parameters in real time, before a coil is committed to scrap. It is the AI platform monitoring ten thousand retail store endpoints for anomalous access patterns. It’s the kind of physical security intelligence that previously required a team of analysts reviewing footage after the fact. It is the building management system that learns occupancy patterns, weather forecasts, and energy pricing in real time and adjusts HVAC loads accordingly. None of these are narrow industrial problems. All of them are operational ones.

AI Enables Uniquely Deep Competitive Moats for Industrial and Operational Tech Companies

The moats in operational technology are not being built from data alone, they are built from the combination of domain expertise and AI, and it is the combination that is so powerful. A generalist AI vendor can build a capable anomaly detection model. What they cannot easily replicate is a vendor who has spent fifteen years embedded in metal fabrication, who knows that a particular vibration signature at a specific spindle speed means a tool is about to fracture rather than simply wear, and who has encoded that understanding into a model trained on tens of millions of cycles across hundreds of production environments. The AI is the amplifier. The domain knowledge is what makes the signal meaningful. This dynamic plays out across every operational vertical. A logistics technology vendor that deeply understands the physical constraints of pick-path optimization can build AI models that a pure software company, however technically sophisticated, would take years to match. The domain expertise defines the feature space, shapes the training data, and determines which model outputs are operationally actionable versus theoretically correct but practically useless. Without it, even a well-trained model produces recommendations that experienced operators rightly ignore. With it, the model earns trust quickly and embeds itself into daily operations in ways that become very difficult to displace.

The result is an ever deeper and wider moat for the supplier. Each deployment generates proprietary operational data that makes the model sharper. A sharper model earns deeper integration into customer workflows. Deeper integration generates richer data. And because the domain expertise required to interpret and act on that data took years to accumulate, a new entrant cannot shortcut the process simply by acquiring more compute. The combination of hard-won industry knowledge, proprietary training data, and operational embedding creates a defensibility that pure software businesses have rarely been able to achieve.

The industrial and operational tech opportunity remains largely under-penetrated, with AI further enhancing already strong value propositions. There exists a sizeable gap between what can now be accomplished with AI and what is actually deployed.

While The SaaS Opportunity is Heavily Penetrated, Industrial Tech Markets Remains Largely Untapped

Part of what makes the operational tech opportunity so significant is simply how little of it has been captured. Enterprise software has had decades of focused investment and relentless iteration. Every major SaaS category has been competed to exhaustion. Operational technology has not. A mid-sized discrete manufacturer may run an ERP system and a basic MES, but its quality inspection process still relies on manual visual checks that miss defects at speed. A large automotive supplier may have real-time line throughput data but no AI layer identifying which combination of upstream process variables such as temperature drift, tooling wear, raw material batch variation is quietly degrading yield two shifts before a scrap spike appears. A food and beverage plant may track OEE but have no model predicting which packaging line configuration, given today’s SKU mix and ambient humidity, will minimize changeover time. The gap between what is technically possible today and what is actually deployed is enormous, and that gap is opportunity.

AI Will Further Enhance Industrial and Operational Tech Value Propositions

The economics are compelling in a way that pure software economics rarely are. When an AI model detects the early thermal signature of a failing CNC spindle and schedules maintenance before it seizes, the avoided downtime on a high-utilization line can be worth hundreds of thousands of dollars per incident. When computer vision running inline on a circuit board assembly line catches solder defects that previously escaped to end-of-line test, the reduction in rework and scrap is immediate and auditable. When AI-driven process optimization on an injection molding floor reduces cycle time by two percent across a thousand molds, the compounding effect on annual output is substantial and permanent. These are not productivity gains measured in minutes saved per knowledge worker. They are large, discrete, measurable improvements in the unit economics of physical production.

An Aging and Shrinking Industrial Workforce Further Supports the Value of AI

There is also a demographic tailwind that is rarely discussed in the context of AI but is quietly one of the most powerful forces behind operational technology adoption. The skilled workforce that operates physical assets, such as the process engineers who know from experience which subtle cues precede a furnace campaign going off-spec, is retiring faster than it can be replaced. This is happening within a context of an industrial workforce that is already insufficient to meet employer’s needs. AI is not simply automating critical roals roles. In many cases it is preserving institutional knowledge that would otherwise walk out the door permanently. A model trained on the diagnostic reasoning of a thirty-year process engineer captures something genuinely irreplaceable. That kind of knowledge transfer, encoded and deployed at scale, is a new category of value that operational AI uniquely enables.

A Hardware-Enabled Paradigm

For decades, operational data flowed in one direction: from wherever it was generated up to centralized systems where it was stored, analyzed, and acted upon — usually too late to matter. AI at the edge is reversing that logic entirely. By embedding intelligence directly into the devices, sensors, and endpoints where data is born, edge AI eliminates the latency, reliability, bandwidth costs, and privacy issues that makes centralized analysis impractical for real-time decisions. A mission-critical retail computer vision system detecting suspicious behavior could consume untold bandwidth and be subject to high latency and poor reliability if it used cloud-based AI. Indeed, many of the world’s most consequential operational environments, from sprawling retail chains to distributed healthcare facilities to large campus properties, have inconsistent or bandwidth-constrained connections that cloud-first architectures quietly struggle with. Edge AI makes those environments intelligent regardless. What makes the industrial and operational world particularly well-positioned for this shift is that the hardware infrastructure – along with the right customer mindset – is largely already there. On-site servers, smart cameras, point-of-sale systems, and purpose-built edge gateways are already deployed across warehouses, retail floors, and facilities. They were put there to run operational systems, and increasingly they have more than enough compute headroom to run sophisticated AI models alongside them. The edge AI revolution in industrial and operational tech often doesn’t require a wholesale hardware refresh; it requires software and models intelligent enough to take advantage of what’s already installed. As those models grow more efficient and edge hardware more capable, the result is a new class of operational technology that is faster, more resilient, and more deeply embedded in the physical world than anything that came before it. It will not be lost on suppliers or investors that, once deployed, the challenges associated with hardware replacement adds to the stickiness of industrial and operational tech customer relationships.

Industrial tech is by its very nature a hardware-centric sector. This creates the infrastructure to enable high value edge-AI applications, and can drive unusually strong customer retention.

Industrial and Operational Tech Will Present a New Compelling Opportunity for Disillusioned SaaS Investors

What is unfolding across operational and industrial technology is not simply a shift in which software vendors are ascendant, it is a fundamental expansion in what physical industries can do. Retail environments that once absorbed shrink as an unavoidable cost of doing business are deploying computer vision and behavioral AI that detect theft patterns, organized retail crime networks, and inventory discrepancies in real time, turning loss prevention from a reactive, labor-intensive function into a proactive operational capability. Supply chains that were managed through experience and intuition are becoming genuinely adaptive systems. Infrastructure that degraded on fixed maintenance schedules is learning to signal its own needs. The aggregate effect, across logistics, energy, facilities, retail, and the broader operational world is a step change in the productive capacity of the physical economy.

Ultimately, we believe we are in the early days of a multi-year cycle that will have capital rotating out of SaaS and at least partially into industrial tech. As AI further enhances industrial tech’s already strong value proposition, AI-enabled industrial tech companies are likely to see their margins expand and their growth accelerate. This is almost certain to attract additional capital to industrial tech, some of which would have otherwise gone to SaaS, with corresponding growth in industrial tech valuations. AI did not create the complexity that is industrial tech. It has, for the first time, given companies the tools they need to master it.